Statement of Financial Information Approval and Consolidated Financial Statements

Audited consolidated financial statements for the Town of View Royal as of December 31, 2013.

Town of View Royal

Statement of Financial Information Approval

For the year ended December 31, 2013

The undersigned, as authorized by the Financial Information Regulation, Schedule 1, subsection 9(2), approves all the statements and schedules included in this Statement of Financial Information, produced under the Financial Information Act.

Jeannie Beauchamp, CPA, CGA Director of Finance July 15, 2014

On behalf of Council, Graham Hill, Mayor July 15, 2014

Prepared pursuant to the Financial Information Regulation, Schedule 1, subsection 9

Consolidated Financial Statements of TOWN OF VIEW ROYAL

Year ended December 31, 2013

TOWN OF VIEW ROYAL

Consolidated Financial Statements

Year ended December 31, 2013

Financial Statements

- Management's Responsibility for the Consolidated Financial Statements

- Independent Auditors' Report

- Consolidated Statement of Financial Position

- Consolidated Statement of Operations

- Consolidated Statement of Change in Net Financial Assets

- Consolidated Statement of Cash Flows

- Notes to Consolidated Financial Statements

MANAGEMENT'S RESPONSIBILITY FOR THE CONSOLIDATED FINANCIAL STATEMENTS

The accompanying consolidated financial statements of the Town of View Royal (the "Town") are the responsibility of Town's management and have been prepared in compliance with legislation, and in accordance with Canadian public sector accounting standards for local governments as recommended by the Public Sector Accounting Board of The Canadian Institute of Chartered Accountants. A summary of the significant accounting policies are described in the notes to the consolidated financial statements. The preparation of financial statements necessarily involves the use of estimates based on management's judgment, particularly when transactions affecting the current accounting period cannot be finalized with certainty until future periods.

The Town's management maintains a system of internal controls designed to provide reasonable assurance that assets are safeguarded, transactions are properly authorized and recorded in compliance with legislative and regulatory requirements, and reliable financial information is available on a timely basis for preparation of the consolidated financial statements. These systems are monitored and evaluated by management.

Mayor and Council meet with management and the external auditors to review the consolidated financial statements and discuss any significant financial reporting or internal control matters prior to their approval of the consolidated financial statements.

The consolidated financial statements have been audited by Hayes Stewart Little & Company Chartered Accountants, independent external auditors appointed by the Town. The accompanying Independent Auditors' Report outlines their responsibilities, the scope of their examination and their opinion on the Town's consolidated financial statements. Their opinion is based upon an examination conducted in accordance with Canadian generally accepted auditing standards, performing such tests and other procedures as they consider necessary to obtain reasonable assurance that the consolidated financial statements are free of material misstatement and present fairly the financial position and results of the Town in accordance with Canadian public sector accounting standards.

INDEPENDENT AUDITOR'S REPORT

To the Mayor and members of Council of THE TOWN OF VIEW ROYAL

Report on Consolidated Financial Statements We have audited the accompanying consolidated financial statements of the Town of View Royal, which comprise the consolidated statement of financial position as at December 31, 2013, and the consolidated statement of operations, change in net financial assets, and cash flows for the year then ended, and a summary of significant accounting policies and other explanatory information.

Management's Responsibility for the Consolidated Financial Statements Management is responsible for the preparation and fair presentation of these consolidated financial statements in accordance with Canadian public sector accounting standards and for such internal control as management determines is necessary to enable the preparation of consolidated financial statements that are free from material misstatement, whether due to fraud or error.

Auditor's Responsibility Our responsibility is to express an opinion on these consolidated financial statements based on our audit. We conducted our audit in accordance with Canadian generally accepted auditing standards. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the consolidated financial statements are free of material misstatement, whether due to fraud or error.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the consolidated financial statements. The procedures selected depend on the auditor's judgment, including the assessment of the risks of material misstatement of the consolidated financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity's preparation and fair presentation of the consolidated financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluation of the overall presentation of the consolidated financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Opinion In our opinion, these consolidated financial statements present fairly, in all material respects, the financial position of the Town of View Royal as at December 31, 2013 and its financial performance, changes in net financial assets and its cash flow for the year then ended in accordance with Canadian public sector accounting standards.

Other Matter The financial statements for the year ended December 31, 2012 were audited by another accounting firm and are presented for comparative purposes only.

Victoria, BC May 6, 2014

Chartered Accountants

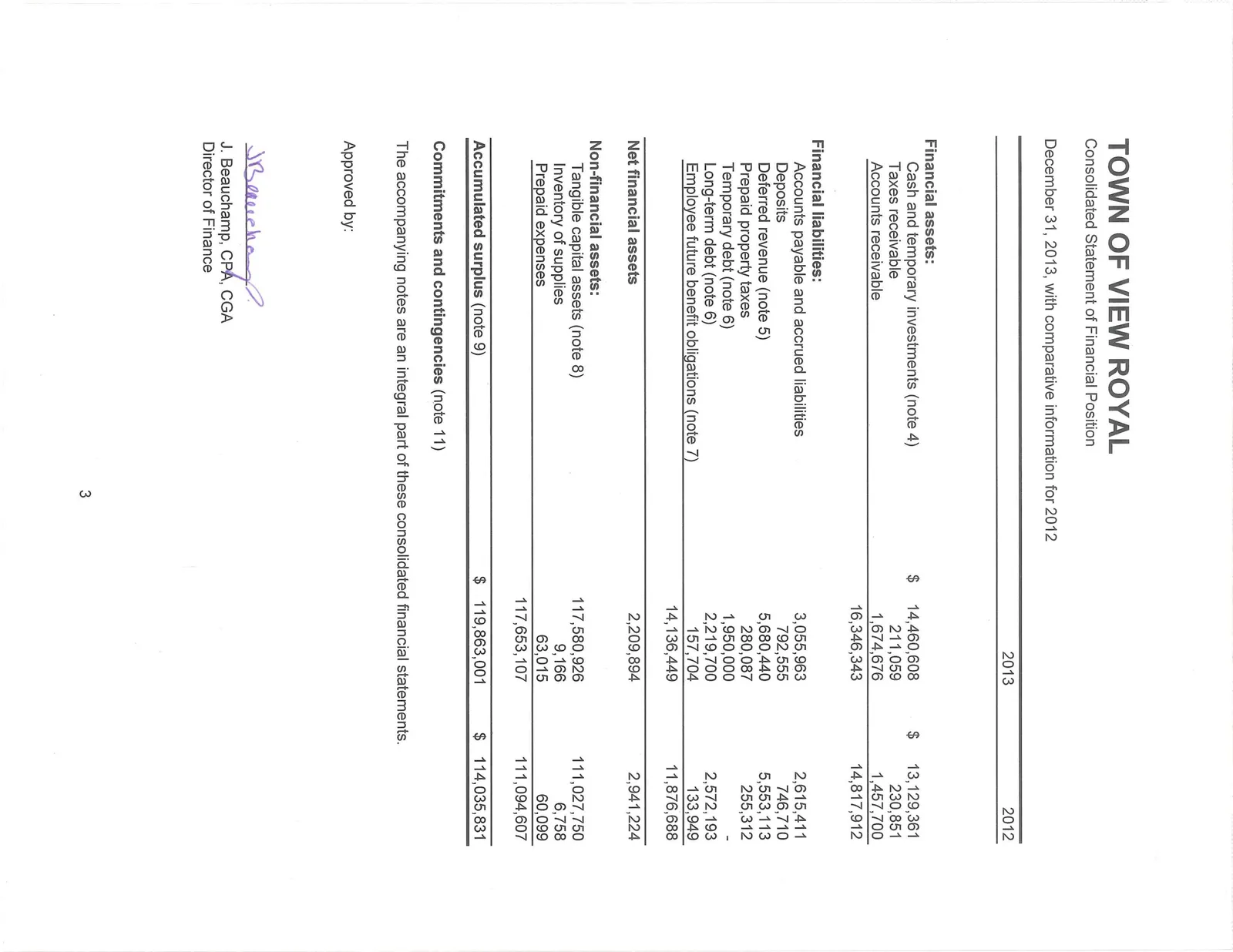

TOWN OF VIEW ROYAL

Consolidated Statement of Financial Position

December 31, 2013, with comparative information for 2012

| 2013 | 2012 | |

|---|---|---|

| Financial assets: | ||

| Cash and temporary investments (note 4) | $ 14,460,608 | $ 13,129,361 |

| Taxes receivable | 211,059 | 230,851 |

| Accounts receivable | 1,674,676 | 1,457,700 |

| 16,346,343 | 14,817,912 | |

| Financial liabilities: | ||

| Accounts payable and accrued liabilities | 3,055,963 | 2,615,411 |

| Deposits | 792,555 | 746,710 |

| Deferred revenue (note 5) | 5,680,440 | 5,553,113 |

| Prepaid property taxes | 280,087 | 255,312 |

| Temporary debt (note 6) | 1,950,000 | - |

| Long-term debt (note 6) | 2,219,700 | 2,572,193 |

| Employee future benefit obligations (note 7) | 157,704 | 133,949 |

| 14,136,449 | 11,876,688 | |

| Net financial assets | 2,209,894 | 2,941,224 |

| Non-financial assets: | ||

| Tangible capital assets (note 8) | 117,580,926 | 111,027,750 |

| Inventory of supplies | 9,166 | 6,758 |

| Prepaid expenses | 63,015 | 60,099 |

| 117,653,107 | 111,094,607 | |

| Accumulated surplus (note 9) | $ 119,863,001 | $ 114,035,831 |

TOWN OF VIEW ROYAL

Consolidated Statement of Operations

Year ended December 31, 2013, with comparative information for 2012

| Financial plan (note 12) | 2013 | 2012 | |

|---|---|---|---|

| Revenues: | |||

| Taxation, net (note 10) | $ 6,046,456 | $ 6,026,329 | $ 5,679,365 |

| User charges | 2,490,338 | 2,424,127 | 2,319,314 |

| Government transfers: | |||

| Provincial | 2,803,121 | 2,045,306 | 3,039,415 |

| Federal | 6,050,598 | 5,559,410 | 661,530 |

| Municipal | - | 5,661 | 30,989 |

| Investment income | 65,000 | 119,924 | 132,157 |

| Actuarial adjustment to debt | - | 46,109 | 45,861 |

| Penalties and fines | 52,000 | 57,520 | 56,068 |

| Development charges earned | 115,000 | 130,673 | 21,837 |

| Contributions from developers and others | - | 1,327,863 | 53,243 |

| Other revenue from own sources | 74,973 | 156,871 | 109,419 |

| Total revenues | 17,697,486 | 17,899,793 | 12,149,198 |

| Expenses: | |||

| General government | 1,973,035 | 1,892,080 | 1,823,602 |

| Protective services | 3,119,524 | 2,997,631 | 3,069,369 |

| Transportation services | 3,857,935 | 3,617,656 | 3,567,647 |

| Environmental health services | 990,407 | 848,684 | 1,031,374 |

| Planning and development | 446,232 | 413,703 | 453,625 |

| Recreation and cultural | 2,343,242 | 2,302,869 | 2,704,935 |

| Total expenses | 12,730,375 | 12,072,623 | 12,650,552 |

| Annual surplus (deficit) | 4,967,111 | 5,827,170 | (501,354) |

| Accumulated surplus, beginning of year | 114,035,831 | 114,035,831 | 114,537,185 |

| Accumulated surplus, end of year (note 9) | $ 119,002,942 | $ 119,863,001 | $ 114,035,831 |

TOWN OF VIEW ROYAL

Consolidated Statement of Change in Net Financial Assets

Year ended December 31, 2013, with comparative information for 2012

| Financial plan (note 12) | 2013 | 2012 | |

|---|---|---|---|

| Annual surplus (deficit) | $ 4,967,111 | $ 5,827,170 | $ (501,354) |

| Acquisition of tangible capital assets | (11,510,744) | (8,600,614) | (2,139,078) |

| Contributions of tangible capital assets | - | (336,703) | (6,000) |

| Amortization of tangible capital assets | 2,430,000 | 2,569,502 | 2,567,726 |

| Loss on disposal and write-down of tangible capital assets | - | 14,389 | 92,351 |

| Change in proportionate share of West Shore | - | (199,750) | 231,149 |

| (9,080,744) | (6,553,176) | 746,148 | |

| Acquisition and consumption of inventory of supplies | - | (2,408) | (606) |

| Acquisition and consumption of prepaid expenses | - | (2,916) | (42,627) |

| Change in net financial assets | (4,113,633) | (731,330) | 201,561 |

| Net financial assets, beginning of year | 2,941,224 | 2,941,224 | 2,739,663 |

| Net financial assets, end of year | $ (1,172,409) | $ 2,209,894 | $ 2,941,224 |

TOWN OF VIEW ROYAL

Consolidated Statement of Cash Flows

Year ended December 31, 2013, with comparative information for 2012

| 2013 | 2012 | |

|---|---|---|

| Cash provided by (used in): | ||

| Operating activities: | ||

| Annual surplus (deficit) | $ 5,827,170 | $ (501,354) |

| Items not involving cash: | ||

| Amortization of tangible capital assets | 2,569,502 | 2,567,726 |

| Loss on disposal and write-down of tangible capital assets | 14,389 | 92,351 |

| Contributions of tangible capital assets | (336,703) | (6,000) |

| Change in employee benefits obligations | 23,755 | 12,293 |

| Change in proportionate share of West Shore | (199,750) | 231,149 |

| Actuarial adjustment on debt | (46,109) | (45,861) |

| Changes in non-cash operating assets and liabilities: | ||

| Accounts receivable | (216,976) | 150,137 |

| Taxes receivable | 19,792 | (18,168) |

| Accounts payable and accrued liabilities | 440,552 | 174,907 |

| Deposits | 45,845 | (297,397) |

| Deferred revenue | 127,327 | (166,032) |

| Prepaid property taxes | 24,775 | 26,233 |

| Inventory of supplies | (2,408) | (606) |

| Prepaid expenses | (2,916) | (42,627) |

| 8,288,245 | 2,176,751 | |

| Capital activities: | ||

| Acquisition of tangible capital assets | (8,600,614) | (2,139,077) |

| (8,600,614) | (2,139,077) | |

| Financing activities: | ||

| Debt issued | 1,950,000 | - |

| Debt repaid | (306,384) | (308,289) |

| 1,643,616 | (308,289) | |

| Increase (decrease) in cash and cash equivalents | 1,331,247 | (270,615) |

| Cash and temporary investments, beginning of year | 13,129,361 | 13,399,976 |

| Cash and temporary investments, end of year | $ 14,460,608 | $ 13,129,361 |

TOWN OF VIEW ROYAL

Notes to Consolidated Financial Statements

Year ended December 31, 2013

Town of View Royal (the "Town") is a municipality in the Province of British Columbia and operates under the provisions of the Local Government Act and the Community Charter of British Columbia. The Town's principal activities include the provision of local government services to residents of the incorporated area.

1. Significant accounting policies:

The consolidated financial statements of the Town are prepared by management in accordance with Canadian public sector accounting principles for governments as recommended by the Public Sector Accounting Board ("PSAB") of the Canadian Institute of Chartered Accountants. Significant accounting policies adopted by the Town are as follows:

(a) Reporting entity: The consolidated financial statements reflect the combination of all the assets, liabilities, revenues, expenses, and changes in fund balances and in financial position of the Town. The consolidated financial statements of the Town include the Town's proportionate interest in West Shore Parks and Recreation Society ("West Shore"), an organization jointly controlled by the Town. The Town does not administer any trust activities on behalf of external parties other than the disbursement of casino revenues to other municipal partners as described in note 5.

(b) Basis of accounting: The Town follows the accrual method of accounting for revenues and expenses. Revenues are normally recognized in the year in which they are earned and measurable. Expenses are recognized as they are incurred and measurable as a result of receipt of goods or services and/or the creation of a legal obligation to pay. Expenses paid in the current period and attributable to a future period are recorded as prepaid.

(c) Revenue recognition: (i) Taxation revenues are recognized at the time of issuing the property tax notices for the fiscal year. (ii) Sale of services and user fee revenues are recognized when the service or product is rendered by the Town and the amounts are received or become receivable. (iii) Grant revenues are recognized when the funding becomes receivable. (iv) Revenue unearned in the current period is recorded as deferred revenue. (v) Government transfers are recognized in the consolidated financial statements as revenues in the period in which events giving rise to the transfer occur, providing the transfers are authorized, any eligibility criteria have been met, and reasonable estimates of the amounts can be made. Transfers received for which expenses are not yet incurred are included in deferred revenue.

(d) Deferred revenue: Deferred revenue includes grants, contributions and other amounts received from third parties pursuant to legislation, regulation and agreement which may only be used in certain programs, in the completion of specific work, or for the purchase of tangible capital assets. In addition, certain user charges and fees are collected for which the related services have yet to be performed. Revenue is recognized in the period when the related expenses are incurred, services performed, or the tangible capital assets are acquired.

Development cost charges are amounts which are restricted by government legislation or agreement with external parties. When qualifying expenses are incurred development cost charges are recognized as revenue in amounts which equal the associated expenses.

Casino revenues are required to be spent on eligible expenses as defined in the agreement with the provincial government. The gross revenue received is deferred and recorded as revenue when the related expenses are incurred.

(e) Cash and temporary investments: Cash and temporary investments include investments in the Municipal Finance Authority of British Columbia ("MFA") Money Market, Intermediate, and Short-Term Bond that are recorded at cost plus earnings reinvested in the funds, which at December 31, 2013 would approximate market value. These temporary investments consist of cash on deposit in the MFA investment funds that are highly liquid, readily convertible to cash, and are subject to an insignificant risk of change in value.

Investment income is reported as revenue in the period earned. When required by the funding government or related Act, investment income earned on deferred revenue is added to the investment and forms part of the deferred revenue balance.

(f) Deposits: Receipts restricted by third parties are deferred and reported as deposits and are refundable under certain circumstances. Deposits that are prepayments are recognized as revenue when qualifying expenditures are incurred.

(g) Temporary and long-term debt: Temporary and long-term debt is recorded net of related actuarial adjustments and principal repayments.

(h) Employee future benefits: The Town and its employees make contributions to the Municipal Pension Plan. The Town's contributions are expensed as incurred and are included within the Statement of Operations.

Sick leave and other retirement benefits are also available to the Town's employees. The costs of these benefits are actuarially determined based on service and best estimates of retirement ages and expected future salary and wage increases. The obligations under these benefit plans are accrued based on projected benefits as the employees render services necessary to earn the future benefits.

(i) Non-financial assets: Non-financial assets are not available to discharge existing liabilities and are held for use in the provision of services. They have useful lives extending beyond the current year and are not intended for sale in the ordinary course of operations. The change in non-financial assets during the year, together with the excess of revenues over expenses, provides the change in net financial assets for the year.

(i) Tangible capital assets: Tangible capital assets are recorded at cost which includes amounts that are directly attributable to acquisition, construction, development or betterment of the asset. The cost, less residual value, of the tangible capital assets, excluding land, are amortized on a straight line basis over their estimated useful lives as follows:

| Asset | Useful life - years |

|---|---|

| Land | Indefinite |

| Land improvements | 15 - 25 |

| Buildings | 20 - 70 |

| Vehicles, machinery and equipment | 3 - 20 |

| Engineering structures | 10 - 100 |

Amortization is calculated monthly, including in the year of acquisition and disposal. Assets under construction are not amortized until the asset is available for productive use.

Tangible capital assets are written down when conditions indicate that they no longer contribute to the Town's ability to provide goods and services, or when the value of future economic benefits associated with the asset are less than the book value of the asset.

(ii) Contributions of tangible capital assets: Tangible capital assets received as contributions are recorded at their fair value at the date of receipt and also are recorded as revenue.

(iii) Works of art, and historical treasures: The Town manages and controls various works of art and non-operational historical cultural assets including buildings, artifacts, paintings and sculptures located at Town sites and public display areas. These assets are not recorded as tangible capital assets and are not amortized due to the subjectivity of their value.

(iv) Interest capitalization: The Town does not capitalize interest costs associated with the acquisition or construction of a tangible capital asset.

(v) Leased tangible capital assets: Leases which transfer substantially all of the benefits and risks incidental to ownership of property are accounted for as leased tangible capital assets. All other leases are accounted for as operating leases and the related payments are charged to expenses as incurred.

(vi) Inventory of supplies: Inventory of supplies held for consumption is recorded at the lower of cost and replacement cost.

(j) Use of estimates: The preparation of financial statements in conformity with Canadian public sector accounting standards requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities, and disclosure of contingent assets and liabilities at the date of the financial statements, and the reported amounts of revenues and expenses during the period. Significant areas requiring the use of management estimates relate to the determination of accrued sick benefits liability, collectability of accounts receivable, amortization of capital assets, deferred charges and provisions for contingencies. Actual results could differ from those estimates. Adjustments, if any, will be reflected in operations in the period of settlement.

2. Financial instruments:

The Town’s financial instruments consist of cash and temporary investments, accounts receivable, accounts payable and accrued liabilities, deposits, and temporary and long-term debt. The carrying amount of these financial instruments approximates their fair value because they are short-term in nature or because they bear interest at market rates.

Unless otherwise noted, it is management’s opinion that the Town is not exposed to significant interest or credit risks arising from these financial instruments.

3. Future accounting changes:

(a) PS 3260 – Liability for contaminated sites: This section establishes the recognition, measurement and disclosure requirements for reporting liabilities associated with remediation of contaminated sites. The section does not deal with tangible capital asset retirement obligations, liabilities associated with the disposal or sale of a tangible capital asset and acquisition/ betterment costs for tangible capital assets that are less than the future economic benefits. This section applies to fiscal years beginning on or after April 1, 2014, with early adoption permitted.

(b) PS 3450 – Financial instruments: This section establishes standards for recognizing and measuring financial assets, financial liabilities and non-financial derivatives. This section applies to fiscal years beginning on or after April 1, 2016, with early adoption permitted.

(c) PS 2601 – Foreign currency translation: This section revises and replaces the existing Section PS 2600 Foreign currency translation. This section applies to fiscal years beginning on or after April 1, 2016, with early adoption permitted.

(d) PS 1201 – Financial statement presentation: This section revises and replaces the existing Section PS 1200 Financial statement presentation. This section applies to fiscal years beginning on or after April 1, 2016, with early adoption permitted.

4. Cash and temporary investments:

| 2013 | 2012 | |

|---|---|---|

| Bank deposits | $ 2,573,156 | $ 2,142,738 |

| Municipal Finance Authority – Money Market | 5,343,821 | 4,861,442 |

| Municipal Finance Authority – Intermediate | 1,599,525 | 1,576,831 |

| Municipal Finance Authority – Short-Term Bond | 4,944,106 | 4,548,350 |

| $ 14,460,608 | $ 13,129,361 |

Temporary investments consist of short-term investments in the MFA money market, intermediate, and short-term bond funds. The market value is equal to the carrying value. Temporary investments have yields ranging from 1.10% to 1.70%.

Included in cash and temporary investments are the following restricted amounts:

| 2013 | 2012 | |

|---|---|---|

| Restricted cash – MFA | $ 26,716 | $ 44,927 |

| Restricted cash – West Shore reserve funds | 250,992 | 209,160 |

| Restricted investments – reserve funds | 2,921,742 | 2,951,801 |

| Restricted investments – development cost charges | 4,231,743 | 4,258,174 |

| $ 7,431,193 | $ 7,464,062 |

The Town has an operating line of credit with the Bank of Nova Scotia for an authorized amount of $400,000, bearing interest at bank prime rate plus 0.25% per annum with interest payable monthly. At December 31, 2013 the balance outstanding was $nil (2012 - nil).

5. Deferred revenue:

The Town has entered into an agreement with the Province whereby 10% of the net gaming revenue from community casinos is to be paid to local governments. The Town has also entered into a casino revenue sharing agreement with neighbouring municipalities whereby 55% of the revenue received from the Province in respect of the gaming facility situated within the Town is to be disbursed to these governments. The disbursement of the 55% is netted against the revenue in the financial statements for the Town and is disclosed below as a disbursement to other municipal partners.

| 2013 | 2012 | |

|---|---|---|

| Gaming revenue: | ||

| Deferred net gaming revenue, beginning of year | $ 698,089 | $ 1,174,734 |

| Amounts received during the year | 4,161,177 | 4,158,126 |

| Disbursements: | ||

| Eligible expenditures | (1,684,219) | (2,347,802) |

| Other municipal partners | (2,288,648) | (2,286,969) |

| Deferred net gaming revenue, end of year | 886,399 | 698,089 |

| Federal Gas Tax Agreement Funds: | ||

| Deferred gas tax agreement funds, beginning of year | 247,512 | 320,548 |

| Amounts received during the year | 285,526 | 285,635 |

| Interest earned | 3,197 | 5,455 |

| Eligible expenses | (448,726) | (364,126) |

| Deferred gas tax agreement funds, end of year | 87,509 | 247,512 |

| Development cost charges: | ||

| Deferred development cost charges, beginning of year | 4,258,174 | 3,869,055 |

| Amounts received during the year | 49,466 | 340,296 |

| Interest earned | 54,776 | 70,660 |

| Eligible expenses | (130,673) | (21,837) |

| Deferred development cost charges, end of year | 4,231,743 | 4,258,174 |

| Deferred revenue - other | 474,789 | 349,338 |

| Total deferred revenue | $ 5,680,440 | $ 5,553,113 |

6. Temporary and long-term debt:

(a) Temporary debt (interim financing) of $1,950,000 was issued in 2013 by the MFA related to the construction of the new Public Safety Building. The temporary debt is due on demand and has an interest rate of 1.72%. Interest is calculated daily and compounded and paid monthly. In 2014 it is expected that this debt will be repaid and replaced with long-term debt issued by the MFA.

(b) Included in long-term debt is the Town's proportionate share of a West Shore five year fixed rate term loan for $23,796 (2012 - $36,076).

(c) Debt outstanding:

| MFA Issue Number | Interest rate | Maturity date | Originally Approved | Net debt 2013 | Net debt 2012 |

|---|---|---|---|---|---|

| 95 | 4.07% | Oct 13, 2013 | $1,493,000 | $ - | $ 213,223 |

| 117 | 3.25% | Oct 12, 2026 | 2,445,000 | 2,195,904 | 2,322,894 |

| West Shore Parks & Recreation | 23,796 | 36,076 | |||

| $ 3,938,000 | $ 2,219,700 | $ 2,572,193 |

(d) Debenture debt: The loan agreements with the Capital Regional District and the MFA provide that if, at any time, the scheduled payments provided for in the agreements are not sufficient to meet the MFA’s obligations in respect of such borrowings, the resulting deficiency becomes a liability of the Town.

The Town issues its debt instruments through the MFA. Debt is issued on a sinking fund basis, where the MFA invests the Town’s sinking fund principal payments so that the payments, plus investment income, will equal the original outstanding debt amount at the end of the repayment period. Actuarial adjustments on debt represent the repayment and/or forgiveness of debt by the MFA using surplus investment income generated by the principal repayments.

Principal payments on long-term debt for the next five years are as follows:

| Year | Total |

|---|---|

| 2014 | $ 122,106 |

| 2015 | 122,106 |

| 2016 | 122,106 |

| 2017 | 122,106 |

| 2018 | 122,106 |

(e) Interest expense: Total interest expense during the year was $133,093 (2012 - $140,275).

7. Employee future benefit obligations:

Employee benefit obligations represent accrued benefits as follows:

| 2013 | 2012 | |

|---|---|---|

| Vacation payable | $ 43,204 | $ 25,893 |

| Accrued overtime | 15,826 | 13,995 |

| Sick leave entitlements | 53,000 | 53,400 |

| West Shore employee future benefit obligations | 45,674 | 40,661 |

| $ 157,704 | $ 133,949 |

Accrued vacation is the amount of unused vacation entitlement carried forward into the next year. Accrued sick leave is the estimated liability for sick leave for all employees. Sick leave entitlements can only be used while employed by the Town and are not paid out upon retirement or termination of employment. The accrued sick leave cost was estimated by an actuarial valuation completed effective for December 31, 2013.

Information about liabilities for accrued sick leave is as follows:

| 2013 | 2012 | |

|---|---|---|

| Accrued benefit liability, beginning of year | $ 53,400 | $ 33,700 |

| Current service cost | 8,600 | 6,600 |

| Interest cost | 2,200 | 1,400 |

| Benefits paid | (200) | (200) |

| Amortization of actuarial loss | (11,000) | 11,900 |

| Accrued benefit liability, end of year | $ 53,000 | $ 53,400 |

| 2013 | 2012 | |

|---|---|---|

| Accrued benefit liability, end of year | $ 53,000 | $ 53,400 |

| Unamortized loss | 6,700 | - |

| Accrued benefit obligation, end of year | $ 59,700 | $ 53,400 |

The accrued benefit liability is included as part of employee benefit obligations on the Statement of Financial Position. The actuarial loss is amortized over a period equal to the employees’ average remaining service lifetime of 13 years.

The significant actuarial assumptions adopted in measuring the Town’s accrued benefit obligations are as follows:

| 2013 | 2012 | |

|---|---|---|

| Discount rates | 4.20% | 3.60% |

| Expected future inflation rates | 2.50% | 2.50% |

| Expected wage and salary increases | 2.58 to 4.50% | 2.58 to 4.50% |

Municipal Pension Plan: The Town and its employees contribute to the Municipal Pension Plan (the Plan), a jointly trusteed pension plan. The board of trustees, representing plan members and employers, is responsible for overseeing the management of the Plan, including investment of the assets and administration of benefits. The Plan is a multi-employer contributory pension plan. Basic pension benefits provided are based on a formula. The plan has about 179,000 active members and approximately 71,000 retired members. Active members include approximately 31 contributors from the Town.

The most recent actuarial valuation as at December 31, 2012 indicated a $1,370 million funding deficit for basic pension benefits. The next valuation will be as at December 31, 2015 with results available in 2016. Employers participating in the Plan record their pension expense as the amount of employer contributions made during the fiscal year (defined contribution pension plan accounting). This is because the Plan records accrued liabilities and accrued assets for the Plan in aggregate with the result that there is no consistent and reliable basis for allocating the obligation, assets and cost to the individual employers participating in the Plan.

The Town paid $196,852 (2012 - $181,230) for employer contributions while Town employees contributed $177,090 (2012 - $169,889) to the plan in fiscal 2013.

8. Tangible capital assets:

| Cost (Dec 31, 2012) | Additions | Disposals/ Write-downs/ Change in ownership | Cost (Dec 31, 2013) | Accumulated Amortization (Dec 31, 2012) | Disposals/ Change in ownership | Amortization | Accumulated Amortization (Dec 31, 2013) | Net Book Value (Dec 31, 2012) | Net Book Value (Dec 31, 2013) | |

|---|---|---|---|---|---|---|---|---|---|---|

| Land | $ 37,260,994 | $ 14,333 | $ - | $ 37,275,327 | $ - | $ - | $ - | $ - | $ 37,260,994 | $ 37,275,327 |

| Land Improvements | 2,625,852 | 201,311 | 90,000 | 2,737,163 | 1,564,344 | 77,916 | 99,515 | 1,585,943 | 1,061,508 | 1,151,220 |

| Buildings | 4,783,575 | 23,015 | 106,881 | 4,699,709 | 2,134,957 | 106,881 | 188,091 | 2,216,167 | 2,648,618 | 2,483,542 |

| Vehicles, Machinery and Equipment | 4,181,944 | 1,039,774 | 22,661 | 5,199,057 | 2,455,503 | 22,661 | 327,008 | 2,759,850 | 1,726,441 | 2,439,207 |

| Engineering Structures - General | 69,768,625 | 108,102 | 67,562 | 69,809,165 | 18,633,052 | 67,562 | 1,665,957 | 20,231,447 | 51,135,573 | 49,577,718 |

| Engineering Structures - Sewer | 11,654,053 | 453,334 | - | 12,107,387 | 2,371,430 | - | 122,351 | 2,493,781 | 9,282,623 | 9,613,606 |

| Work In Progress | 1,154,605 | 7,780,990 | 746,592 | 8,189,003 | - | - | - | - | 1,154,605 | 8,189,003 |

| West Shore | 8,596,164 | 63,049 | (240,506) | 8,899,719 | 1,838,776 | (43,060) | 166,580 | 2,048,416 | 6,757,388 | 6,851,303 |

| Total | $ 140,025,812 | $ 9,683,908 | $ 793,190 | $ 148,916,530 | $ 28,998,062 | $ 231,960 | $ 2,569,502 | $ 31,335,604 | $ 111,027,750 | $ 117,580,926 |

(a) Assets under construction and completed assets not yet in service: Assets under construction totaling $8,189,003 (2012 - $1,154,605) have not been amortized. Assets completed but not yet in service totaling $453,335 (2012 – nil) have not been amortized. Amortization of these assets will commence when the asset is put into service.

(b) Contributed tangible capital assets: Contributed tangible capital assets have been recognized at fair market value at the date of contribution. The value of contributed capital assets received during the year is $336,703 (2012 - $6,000).

(c) Tangible capital assets disclosed at nominal values: Where an estimate of fair value could not be made, the tangible capital asset has been recognized at a nominal value.

(d) Write-down of tangible capital assets: The write-down of tangible capital assets during the year was $1,119 (2012 - $37,070).

9. Accumulated surplus:

Accumulated surplus consists of individual fund surplus and reserve funds as follows:

| 2013 | 2012 | |

|---|---|---|

| Surplus: | ||

| Equity in tangible capital assets | $ 113,411,226 | $ 108,455,557 |

| Unrestricted general fund surplus | 1,763,627 | 1,009,089 |

| Unrestricted sewer fund surplus | 1,515,414 | 1,410,224 |

| Total surplus | 116,690,267 | 110,874,870 |

| Reserve funds set aside for specific purposes by Council: | ||

| Capital Works and Land Acquisition | 638,553 | 472,795 |

| Fire Department Equipment | 156,901 | 198,777 |

| Machinery and Equipment Depreciation | 43,105 | 62,951 |

| Municipal Roads Capital | 27,036 | 26,694 |

| Parks and Open Space | 300,670 | 296,869 |

| Parks and Recreation Equipment | 205,208 | 201,425 |

| Police Equipment, Property and Contract | 596,998 | 587,460 |

| Police Operation and Maintenance | 232,779 | 257,830 |

| Road Trust | 117,070 | 115,590 |

| Sewer System Capital | 817,409 | 1,035,644 |

| Sewer System Equipment Replacement | 93,595 | 82,454 |

| Tax Sale Land | 8,418 | 8,312 |

| Internal borrowing | (316,000) | (395,000) |

| West Shore reserves | 250,992 | 209,160 |

| Total reserve funds | 3,172,734 | 3,160,961 |

| $ 119,863,001 | $ 114,035,831 |

10. Net taxes available for municipal purposes:

The Town is required to collect taxes on behalf of and transfer these amounts to the government agencies noted below. Taxes levied over or under the amounts requisitioned are recorded as accounts payable or receivable.

| 2013 | 2012 | |

|---|---|---|

| Taxes | ||

| Property taxes | $ 12,307,265 | $ 11,671,462 |

| Revenues in lieu of taxes | 178,647 | 169,996 |

| 1% utility taxes | 123,871 | 118,693 |

| 12,609,783 | 11,960,151 | |

| Less taxes levied for other authorities: | ||

| School authorities | 4,194,788 | 4,160,901 |

| Capital Regional District | 1,007,289 | 824,794 |

| Capital Regional Hospital District | 631,685 | 610,036 |

| BC Transit | 614,201 | 550,499 |

| BC Assessment Authority | 135,068 | 134,132 |

| Municipal Finance Authority | 423 | 424 |

| 6,583,454 | 6,280,786 | |

| Net taxes available for municipal purposes | $ 6,026,329 | $ 5,679,365 |

11. Commitments and contingencies:

(a) The Capital Regional District ("CRD") debt, under provisions of the Local Government Act, is a direct, joint and several liability of the CRD and each member municipality within the CRD, including the Town.

(b) The Town is a shareholder and member of the Capital Region Emergency Service Telecommunications ("CREST") Incorporated which provides centralized emergency communications, and related public safety information services to municipalities, regional districts, the provincial and federal governments and their agencies, and emergency service organizations throughout the Greater Victoria region and the Gulf Islands. Members’ obligations to share in funding ongoing operations and any additional costs relating to capital assets are to be contributed pursuant to a Members’ Agreement.

(c) The Town is a defendant in various lawsuits. The Town records an accrual in respect of legal claims that are likely to be successful and for which a liability amount is reasonably determinable. The remaining claims, should they be successful as a result of litigation, will be recorded when a liability is likely and determinable. The Town is self-insured through membership in the Municipal Insurance Association of British Columbia. Under this program, member municipalities are to share jointly for general liability claims against any member in excess of $10,000. Should the Association pay out claims in excess of premiums received, it is possible that the Town, along with the other participants, would be required to contribute towards the deficit.

A lawsuit has been initiated against the Town alleging significant financial losses by the claimant as a result of alleged fraudulent misrepresentation by representatives of the Town. The Town has denied these claims and, represented by insurers, is vigorously defending the lawsuit. As the final outcome of the legal action and the potential financial impact to the Town is not determinable, the Town has not recorded any provision for this matter in the financial statements as at December 31, 2013.

(d) Under borrowing arrangements with the MFA, the Town is required to lodge security by means of demand notes and interest-bearing cash deposits based on the amount of the borrowing. As a condition of these borrowings, a portion of the debenture proceeds is withheld by the MFA as a debt reserve fund. These deposits are included in the Town's financial assets as restricted cash and are held by the MFA as security against the possibility of debt repayment default. If the debt is repaid without default, the deposits are refunded to the Town. At December 31, 2013 there were contingent demand notes of $76,334 (2012 - $172,803) which are not included in the financial statements of the Town.

(e) The Town entered into a long-term contract with the Federal Government and the Royal Canadian Mounted Police for the provision of police services. Under the terms of this contract, the Town is responsible for 70% of policing costs. The 2014 estimated cost of this contract is $1,400,812. RCMP members and the federal government are currently in legal proceedings regarding pay raises for 2009 and 2010 that were retracted for RCMP members. As the final outcome of the legal action and the potential financial impact to the Town is not determinable, the Town has not recorded any provision for this matter in the financial statements as at December 31, 2013.

12. Financial plan data:

The budget data presented in these consolidated financial statements is based upon the 2013 operating and capital budgets approved by Council on May 14, 2013, adjusted to reflect West Shore proportionately consolidated budgeted revenues and expenses. The chart below reconciles the approved budget to the budget figures reported in these consolidated financial statements.

| Financial plan amount | |

|---|---|

| Revenues: | |

| Financial plan | $ 16,956,590 |

| West Shore | 740,896 |

| Total revenues | 17,697,486 |

| Expenses: | |

| Financial plan | 12,039,962 |

| West Shore | 690,413 |

| Total expenses | 12,730,375 |

| Annual surplus | $ 4,967,111 |

The annual surplus above represents the planned results of operations prior to budgeted transfers between reserve funds, debt repayments and capital expenditures. Interdepartmental revenues and expenses, having no net impact on the annual surplus, have been removed from the financial plan balances to conform to the presentation required.

13. West Shore Parks and Recreation Society:

(a) Capital asset transfer: The lands and facilities comprising the Juan de Fuca Recreation Centre are owned by the member municipalities (the “Municipalities”) in their proportionate share, as specified in the Co-Owners’ Agreement. The Town became party to the agreement effective January 1, 2007. Future improvements are allocated among the partners as per the cost sharing formula in effect each year for each service or facility, as outlined in a Members’ Agreement. For 2013, the Town’s share of improvements purchased by the Society on its behalf is $13,983 (2012 - $14,810).

Because the cost sharing formula in the Members’ Agreement produces different cost shares for the members from year-to-year, there is a gain or loss on the opening fund balances. In 2013, the Town recorded a gain of $199,750 (2012 - a loss of $231,150).

The repayment of the long-term debt associated with the transferred assets will continue to be a regional function, in accordance with the terms of an Agreement to Transfer between the CRD, the Municipalities and the Society. The debt payments are charged to the Municipalities as part of the CRD’s annual requisition. The maturity dates of the various borrowings range from 2013 through 2014.

The participating Municipalities have each become members in the Society, which was incorporated to provide parks, recreation and community services to the Municipalities under contract. Under terms of an Operating, Maintenance and Management Agreement, the Society is responsible to equip, maintain, manage and operate the facilities located at the recreation centre.

(b) Consolidation: Financial results and budget for the Society are consolidated into the Town’s financial statements proportionately, based on the cost sharing formula outlined in the Members’ Agreement. In 2013, the Town’s proportion for consolidation purposes was 14.125% (2012 - 13.724%). Condensed financial information for the Society is as follows:

| 2013 | 2012 | |

|---|---|---|

| Financial assets | $ 2,993,912 | $ 2,219,968 |

| Financial liabilities | 2,112,249 | 1,658,182 |

| Net financial assets | 881,663 | 561,786 |

| Non-financial assets | 879,243 | 752,357 |

| Accumulated surplus | $ 1,760,906 | $ 1,314,143 |

| Revenues | $ 5,694,277 | $ 5,424,178 |

| Requisition for members | 4,845,294 | 4,698,024 |

| 10,539,571 | 10,122,202 | |

| Expenses | 10,092,808 | 9,820,871 |

| Annual surplus (deficit) | $ 446,763 | $ 301,331 |

14. Segmented information:

The Town is a diversified municipal organization that provides a wide range of services to its citizens. Town services are provided by departments and their activities reported separately. Certain functions that have been separately disclosed in the segmented information, along with the services they provide, are as follows:

General government The general government operations provide the functions of corporate administration, finance, human resources and legislative services and any other functions categorized as non-departmental.

Protective services Protective Services includes the View Royal Fire Rescue which is a paid / composite fire department responsible to provide fire suppression service, fire inspections of public buildings, and training and education of volunteer firemen as well as the citizens of View Royal. In addition, it also includes policing provided by the RCMP, emergency planning, animal control and the maintenance and enforcement of building and construction bylaws as well as all other municipal bylaws. Fire protection services are provided to the Songhees and Esquimalt First Nation communities under contract.

Transportation services Transportation services is comprised of a wide variety of services such as the annual maintenance of all municipally owned roads and bridges, sidewalks, street signage, boulevards, bus shelters, street lighting and traffic signals. Transportation also includes the design, inspection, and maintenance of the storm drain collection systems.

Environmental health services Environmental health services are comprised of the following services:

- Solid Waste Management – providing the service of solid waste collection and disposal to the citizens of View Royal.

- Liquid Waste Management (Sewer) Services – providing the removal of the Town’s waste water (sewage).

Planning and development services Environmental development services include all land use, planning and zoning issues in the Town of View Royal.

Recreation and cultural services Recreation and culture is comprised of services meant to improve the health and development of the citizens of View Royal. This segment includes maintenance and development of all parks and green space within the Town of View Royal as well as the Town's financial contribution to the services provided by the Greater Victoria Public Library and the Town’s portion of West Shore Parks and Recreation Society.

Statement of segmented information The following statement provides additional financial information for the foregoing functions. Certain allocation methodologies have been employed in the preparation of the segmented financial information. Taxation is apportioned based on budgeted taxation revenue as presented in the consolidated financial plan.

The accounting policies used in these segments are consistent with those followed in the preparation of the financial statements as disclosed in Note 1.

2013 Segmented Information Table

| General Government | Protective Services | Transportation Services | Environmental Health Services | Planning and Development Services | Recreation and Cultural Services | Total | |

|---|---|---|---|---|---|---|---|

| Revenues: | |||||||

| Taxation | $ 1,103,155 | $ 1,991,079 | $ 2,357,298 | $ - | $ 352,056 | $ 222,741 | $ 6,026,329 |

| User charges | 12,326 | 271,856 | 36,955 | 1,099,785 | 243,002 | 760,203 | 2,424,127 |

| Developer charges earned | 9,664 | - | - | 115,000 | - | 6,009 | 130,673 |

| Contributions from developers and others | 991,160 | - | - | 336,703 | - | - | 1,327,863 |

| Other revenue from own sources | 57,995 | 63,507 | - | - | - | 35,369 | 156,871 |

| Investment income | 61,994 | 9,576 | 10,223 | 31,640 | - | 6,491 | 119,924 |

| Penalties and fines | 57,520 | - | - | - | - | - | 57,520 |

| Actuarial adjustment to debt | - | 5,998 | 40,111 | - | - | - | 46,109 |

| Government transfers | 411,205 | 265,033 | 5,847,914 | - | - | 1,086,225 | 7,610,377 |

| Total revenues | 2,705,019 | 2,607,049 | 8,292,501 | 1,583,128 | 595,058 | 2,117,038 | 17,899,793 |

| Expenses: | |||||||

| Salaries, wages, and benefits | 991,366 | 1,178,681 | 327,101 | 40,581 | 346,608 | 1,191,775 | 4,076,112 |

| Contracted and general services | 331,914 | 1,303,859 | 1,368,883 | 497,622 | 48,978 | 539,716 | 4,090,972 |

| Materials, supplies, and utilities | 58,729 | 88,811 | 173,197 | 27,037 | 1,122 | 159,793 | 508,689 |

| Other | 355,159 | 139,810 | 9,062 | 15,832 | 14,338 | 359,805 | 894,006 |

| Amortization | 154,912 | 200,990 | 1,691,800 | 267,612 | 2,657 | 251,530 | 2,569,501 |

| Change in proportionate share of West Shore | - | - | - | - | - | (199,750) | (199,750) |

| Debt services | - | 85,480 | 47,613 | - | - | - | 133,093 |

| Total expenses | 1,892,080 | 2,997,631 | 3,617,656 | 848,684 | 413,703 | 2,302,869 | 12,072,623 |

| Annual surplus (deficit) | $ 812,939 | $ (390,582) | $ 4,674,845 | $ 734,444 | $ 181,355 | $ (185,831) | $ 5,827,170 |

2012 Segmented Information Table

| General Government | Protective Services | Transportation Services | Environmental Health Services | Planning and Development Services | Recreation and Cultural Services | Total | |

|---|---|---|---|---|---|---|---|

| Revenues: | |||||||

| Taxation | $ 418,736 | $ 2,185,638 | $ 1,952,288 | $ - | $ 429,000 | $ 693,703 | $ 5,679,365 |

| User charges | 8,638 | 256,593 | 71,487 | 1,041,969 | 248,652 | 691,975 | 2,319,314 |

| Developer charges earned | - | - | - | 21,837 | - | - | 21,837 |

| Contributions from developers and others | 1,243 | - | 6,000 | - | - | 46,000 | 53,243 |

| Other revenue from own sources | 12,252 | 74,131 | - | - | - | 23,036 | 109,419 |

| Investment income | 60,805 | 18,500 | 11,582 | 33,546 | - | 7,724 | 132,157 |

| Penalties and fines | 56,068 | - | - | - | - | - | 56,068 |

| Actuarial adjustment to debt | - | 1,071 | 44,790 | - | - | - | 45,861 |

| Government transfers | 775,712 | 589,434 | 1,221,247 | - | 44,699 | 1,100,842 | 3,731,934 |

| Total revenues | 1,333,454 | 3,125,367 | 3,307,394 | 1,097,352 | 722,351 | 2,563,280 | 12,149,198 |

| Expenses: | |||||||

| Salaries, wages, and benefits | 926,606 | 1,138,750 | 184,032 | 184,032 | 330,304 | 1,154,679 | 3,918,403 |

| Contracted and general services | 282,945 | 1,377,239 | 1,441,751 | 456,360 | 106,095 | 986,462 | 4,650,852 |

| Materials, supplies, and utilities | 83,781 | 105,978 | 169,635 | 30,194 | 1,023 | 80,939 | 471,550 |

| Other | 377,969 | 153,151 | 11,229 | 106,793 | 13,546 | 7,909 | 670,597 |

| Amortization | 152,301 | 214,741 | 1,700,235 | 253,995 | 2,657 | 243,796 | 2,567,725 |

| Change in proportionate share of West Shore | - | - | - | - | - | 231,150 | 231,150 |

| Debt services | - | 79,510 | 60,765 | - | - | - | 140,275 |

| Total expenses | 1,823,602 | 3,069,369 | 3,567,647 | 1,031,374 | 453,625 | 2,704,935 | 12,650,552 |

| Annual surplus (deficit) | $ (490,148) | $ 55,998 | $ (260,253) | $ 65,978 | $ 268,726 | $ (141,655) | $ (501,354) |

15. Comparative figures:

Certain comparative figures have been reclassified to conform to the current year financial statement presentation.