Consolidated Financial Statements - Year ended December 31, 2025

The Town's audited consolidated financial statements, including the statements of financial position, operations, and cash flows.

Consolidated Financial Statements

Town of View Royal

Year ended December 31, 2025

45 View Royal Avenue Victoria, BC Canada V9B 1A6 www.viewroyal.ca

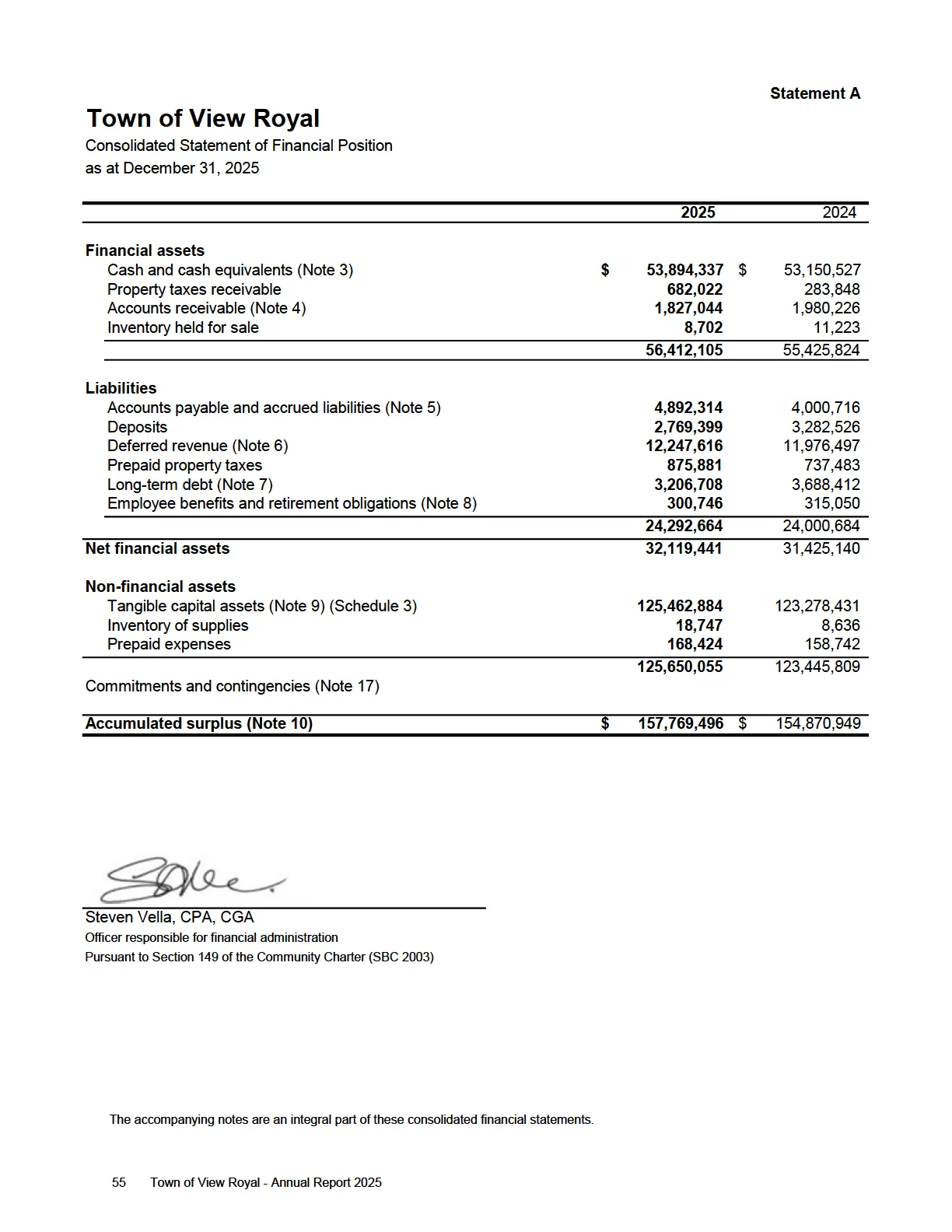

Statement A

Town of View Royal

Consolidated Statement of Financial Position

as at December 31, 2025

| 2025 | 2024 | |

|---|---|---|

| Financial assets | ||

| Cash and cash equivalents (Note 3) | $ 53,894,337 | $ 53,150,527 |

| Property taxes receivable | 682,022 | 283,848 |

| Accounts receivable (Note 4) | 1,827,044 | 1,980,226 |

| Inventory held for sale | 8,702 | 11,223 |

| 56,412,105 | 55,425,824 | |

| Liabilities | ||

| Accounts payable and accrued liabilities (Note 5) | 4,892,314 | 4,000,716 |

| Deposits | 2,769,399 | 3,282,526 |

| Deferred revenue (Note 6) | 12,247,616 | 11,976,497 |

| Prepaid property taxes | 875,881 | 737,483 |

| Long-term debt (Note 7) | 3,206,708 | 3,688,412 |

| Employee benefits and retirement obligations (Note 8) | 300,746 | 315,050 |

| 24,292,664 | 24,000,684 | |

| Net financial assets | 32,119,441 | 31,425,140 |

| Non-financial assets | ||

| Tangible capital assets (Note 9) (Schedule 3) | 125,462,884 | 123,278,431 |

| Inventory of supplies | 18,747 | 8,636 |

| Prepaid expenses | 168,424 | 158,742 |

| 125,650,055 | 123,445,809 | |

| Commitments and contingencies (Note 17) | ||

| Accumulated surplus (Note 10) | $ 157,769,496 | $ 154,870,949 |

Steven Vella, CPA, CGA Officer responsible for financial administration Pursuant to Section 149 of the Community Charter (SBC 2003)

The accompanying notes are an integral part of these consolidated financial statements.

Statement B

Town of View Royal

Consolidated Statement of Operations

Year ended December 31, 2025

| Financial plan (Note 19) | 2025 | 2024 | |

|---|---|---|---|

| Revenue | |||

| Taxes for municipal purposes (Note 14) | $ 13,184,221 | $ 13,033,436 | $ 12,209,528 |

| User charges and sales of services | 5,673,271 | 5,796,531 | 5,842,294 |

| Investment income | 615,000 | 1,386,512 | 2,059,442 |

| Actuarial adjustments on debt | - | 157,361 | 143,633 |

| Penalties and fines | 79,000 | 134,080 | 137,670 |

| Development charges earned | 644,840 | 204,009 | 348,948 |

| Contributions from developers and others | 10,000 | 2,402,471 | 1,049,550 |

| Other revenue from own sources | 265,018 | 157,551 | 503,746 |

| Government grants and transfers (Note 16) | 4,236,265 | 3,257,637 | 3,883,449 |

| Gain (loss) on sale of tangible capital assets (Note 9) | - | 15,082 | (63,566) |

| 24,707,615 | 26,544,670 | 26,114,694 | |

| Expense | |||

| General government services | 3,515,580 | 3,100,913 | 2,902,317 |

| Protective services | 8,134,702 | 7,890,283 | 6,137,187 |

| Transportation services | 5,446,209 | 4,815,302 | 4,852,813 |

| Environmental health services | 3,159,033 | 2,983,098 | 2,871,649 |

| Development services | 994,323 | 946,499 | 709,841 |

| Recreation and cultural services | 3,843,653 | 3,910,028 | 3,973,007 |

| 25,093,500 | 23,646,123 | 21,446,814 | |

| Annual surplus (deficit) | (385,885) | 2,898,547 | 4,667,880 |

| Accumulated surplus, beginning | 154,870,949 | 154,870,949 | 150,203,069 |

| Accumulated surplus, ending | $ 154,485,064 | $ 157,769,496 | $ 154,870,949 |

Statement C

Town of View Royal

Consolidated Statement of Change in Net Financial Assets

Year ended December 31, 2025

| Financial plan (Note 19) | 2025 | 2024 | |

|---|---|---|---|

| Annual surplus (deficit) | $ (385,885) | $ 2,898,547 | $ 4,667,880 |

| Acquisition of tangible capital assets | (7,046,352) | (3,118,021) | (4,753,869) |

| Contributed tangible capital assets | - | (2,395,201) | - |

| Amortization of tangible capital assets | 3,338,711 | 3,272,351 | 3,314,066 |

| (Gain) loss on disposal and write-down of tangible capital assets | - | (15,082) | 63,566 |

| Proceeds on sale of tangible capital assets | - | 10,136 | 35,800 |

| Change in proportionate share of West Shore Parks and Recreation Society | - | 61,364 | 245,655 |

| Change in inventory of supplies | - | (10,111) | 5,962 |

| Change in prepaid expenses | - | (9,682) | (26,052) |

| Increase (decrease) in net financial assets | (4,093,526) | 694,301 | 3,553,008 |

| Net financial assets, beginning | 31,425,140 | 31,425,140 | 27,872,132 |

| Net financial assets, ending | $ 27,331,614 | $ 32,119,441 | $ 31,425,140 |

The accompanying notes are an integral part of these consolidated financial statements.

Statement D

Town of View Royal

Consolidated Statement of Cash Flows

Year ended December 31, 2025

| 2025 | 2024 | |

|---|---|---|

| Cash provided by (used in) | ||

| Operating activities | ||

| Annual surplus | $ 2,898,547 | $ 4,667,880 |

| Items not affecting operating activities | ||

| Amortization of tangible capital assets | 3,272,351 | 3,314,066 |

| (Gain) loss on disposal and write-down of tangible capital assets | (15,082) | 63,566 |

| Change in inventory of supplies | (10,111) | 5,962 |

| Change in prepaid expenses | (9,682) | (26,052) |

| Actuarial adjustment on debt | (148,631) | (142,357) |

| Change in proportionate share of West Shore Parks and Recreation Society | 61,364 | 245,655 |

| Decrease (increase) in non-cash financial assets | ||

| Property taxes receivable | (398,174) | (160,967) |

| Accounts receivable | 153,182 | (4,268) |

| Inventory held for sale | 2,521 | 1,628 |

| Increase (decrease) in liabilities | ||

| Accounts payable and accrued liabilities | 891,598 | (1,044,289) |

| Deposits | (513,127) | 1,036,628 |

| Deferred revenue | 271,119 | 1,030,228 |

| Prepaid property taxes | 138,398 | 43,383 |

| Employee benefits and retirement obligations | (14,304) | 5,466 |

| 4,184,768 | 9,036,529 | |

| Capital activities | ||

| Acquisition of tangible capital assets | (3,118,021) | (4,753,869) |

| Proceeds on disposal of tangible capital assets | 10,136 | 35,800 |

| (3,107,885) | (4,718,069) | |

| Financing activities | ||

| Debt principal repaid | (333,073) | (315,615) |

| Increase in cash and cash equivalents | 743,810 | 4,002,845 |

| Cash and cash equivalents, beginning | 53,150,527 | 49,147,682 |

| Cash and cash equivalents, ending | $ 53,894,337 | $ 53,150,527 |

The accompanying notes are an integral part of these consolidated financial statements.

Town of View Royal

Notes to Consolidated Financial Statements

Year ended December 31, 2025

The Town of View Royal (the "Town") was incorporated on December 5, 1988 by letters patent issued by the Province of British Columbia. Its principal activities are the provision and coordination of local government services to residents of the incorporated area. These services include general government administration, bylaw enforcement, planning and development services, building inspection, fire protection and emergency response planning, public transportation, parks and recreation, solid waste collection and disposal, sewer collection and disposal, and street lighting.

1. Significant accounting policies

a) Principles of consolidation The Town follows Canadian public sector accounting standards. The consolidated financial statements of the Town are prepared in accordance with the recommendations of the Public Sector Accounting Board (PSAB).

b) Reporting entity The consolidated financial statements reflect the combined assets, liabilities, accumulated surplus, revenue and expense of all of the Town's activities and funds. The consolidated financial statements also include the Town's proportionate share of the West Shore Parks and Recreation Society (West Shore). Interfund transactions and fund balances have been eliminated on consolidation.

c) Basis of accounting The Town follows the accrual method of accounting for revenue and expense. Revenue is normally recognized in the year in which it is earned and measurable. Expense is recognized as it is incurred and measurable as a result of receipt of goods or services and/or the creation of a legal obligation to pay. Expense paid in the current period and attributable to a future period is recorded as prepaid expense.

d) Property tax revenue Property tax revenue is recognized at the date property tax notices are issued, based on property assessment values issued by BC Assessment for the current year and tax rates established annually by bylaw. Assessments are subject to appeal and tax adjustments are recorded when the results of appeals are known.

e) Government transfers Government transfers are recognized as revenue in the period the transfers are authorized and any eligibility criteria have been met, except to the extent that transfer stipulations give rise to an obligation that meets the definition of a liability. Transfers are recognized as deferred revenue when transfer stipulations give rise to a liability and recognized in the Consolidated Statement of Operations as revenue as the stipulation liabilities are settled.

1. Significant accounting policies (continued)

f) Revenue recognition User charges and sales of services are recognized as revenue when the performance obligation has been satisfied and when the amount can be estimated and collection is reasonably assured. Deferred revenue is recorded until the performance obligation has been met on these exchange transactions.

For non-exchange transactions, deferred revenue includes grants from non-government sources, contributions and other amounts received from third parties pursuant to legislation, regulation and agreement which may only be used in certain programs, in completion of specific work, or for the purchase of tangible capital assets. Revenue for these non-exchange transactions is recognized when the related expenses are incurred, services performed, or the tangible capital assets are acquired.

Development cost charges are amounts which are restricted by government legislation or agreement with external parties. When qualifying expenses are incurred development cost charges are recognized as revenue in amounts which equal the associated expenses.

g) Investment income Investment income is reported as revenue in the period earned. When required by the funding entity or related legislation, investment income earned on deferred revenue is added to the deferred revenue balance.

h) Cash equivalents Cash equivalents are comprised primarily of Municipal Finance Authority (MFA) pooled investments including money market, intermediate and bond funds. Town funds invested with MFA are pooled with other local governments and are professionally managed and objectively benchmarked by large, secure financial services organizations.

i) Deposits Receipts restricted by third parties are deferred and reported as deposits and are refundable under certain circumstances. Deposits that are prepayments are recognized as revenue when qualifying expenditures are incurred.

j) Employee benefits and retirement obligations The Town and its employees make contributions to the Municipal Pension Plan. The Town’s contributions are expensed as incurred and are included within the Consolidated Statement of Operations.

Sick leave and other retirement benefits are also available to the Town’s employees. The costs of these benefits are actuarially determined based on service and best estimates of retirement ages and expected future salary and wage increases. The obligations under these benefit plans are accrued based on projected benefits as the employees render services necessary to earn the future benefits.

Document Images

(2)